| Acronym | Longform | Definition |

|---|---|---|

| 500-Year Flood | See 0.2-Percent-Annual-Chance Flood | |

| 50-Year Flood | See 2-Percent-Annual-Chance Flood. | |

| Ordinance Level A | Per 44 CFR 60.3 (a), this ordinance level occurs when the Administrator has not defined the special flood hazard areas within a community, has not provided water surface elevation data, and has not provided sufficient data to identify the floodway or coastal high hazard are, but the community has indicated the presence of such hazards by submitting an application to participate in the Program. | |

| Ordinance Level B | Per 44 CFR 60.3 (b), this ordinance level occurs when the Administrator has designated areas of special flood hazards (A zones) by the publication of a community’s FHBM or FIRM, but has neither produced water suface elevation data nor identified a floodway or coastal high hazard area. | |

| Ordinance Level C | Per 44 CFR 60.3 (c), this ordinance level occurs when the Administrator has provided a notice of final flood elevations for one or more special flood hazard areas on the community’s FIRM and, if appropriate, has designated other special flood hazard areas without base flood elevations on the community’s FIRM, but has not identified a regulatory floodway or coastal high hazard area. | |

| Ordinance Level D | Per 44 CFR 60.3 (d), this ordinance level occurs when the Administrator has provided a notice of final flood elevations within Zones A1-30 and/or AE on the community’s FIRM and, if appropriate, has designated AO zones, AH zones, A99 zones, and A zones on the community’s FIRM, and has provided data from which the community shall designate its regulatory floodway. | |

| Ordinance Level E | Per 44 CFR 60.3 (e), this ordinance level occurs when the Administrator has provided a notice of final base flood elevations within Znes A1-30 and/or AE on the community’s FIRM and, if appropriate, has designated AH zones, AO zones, A99 zones, and A zones on the community’s FIRM, and has identified on the community’s FIRM coastal high hazard areas by designating Zones V1-30, and/or V. | |

| Unnumbered A Zone | Flood insurance rate zones, designated “Zone A” on a FIRM, that are based on approximate studies. | |

| zonal classification | Classification based data set value (ranges) and/or material properties or other attributes specified for polygonal regions as is common with GIS products. | |

| SFHA | Special Flood Hazard Area | The area delineated on a National Flood Insurance Program map as being subject to inundation by the base flood. SFHAs are determined using statistical analyses of records of riverflow, storm tides, and rainfall; information obtained through consultation with a community; floodplain topographic surveys; and hydrologic and hydraulic analyses. |

| SOMA | Summary of Map Actions | A list, generated by FEMA and delivered to the community, that summarizes the LOMAs, LOMR-Fs, and LOMRs that are or will be affected by a physical update to a FIRM. |

| SOMA Category 1 | SOMA Category 1 - LOMRs and LOMAs Incorporated | The modifications effected by the LOMRs and LOMAs have been reflected on the Preliminary copies of the revised FIRM panels. However, these LOMRs and LOMAs will remain in effect until the revised FIRM becomes effective. |

| SOMA Category 2 | SOMA Category 2 - LOMRs and LOMAs Not Incorporated (Revalidated) | The modifications effected by the LOMRs and LOMAs have not been reflected on the Preliminary copies of the revised FIRM panels because of scale limitations or because the LOMR or LOMA issued had determined that the lot(s) or structure(s) involved were outside the Special Flood Hazard Area, as shown on the FIRM. These LOMRs and LOMAs will be revalidated free of charge 1 day after the revised FIRM becomes effective through a single letter that reaffirms the validity of the previous LOMC. |

| SOMA Category 3 | SOMA Category 3 - LOMRs and LOMAs Superseded | The modifications effected by the LOMRs and LOMAs have not been reflected on the Preliminary copies of the revised FIRM panels because they are being superseded by new detailed flood hazard information or the information available was not sufficient to make a determination. These LOMRs and LOMAs will no longer be in effect when the revised FIRM becomes effective. |

| SOMA Category 4 | SOMA Category 4 - LOMRs and LOMAs To Be Redetermined | The LOMCs in Category 2 will be revalidated through a single letter that reaffirms the validity of the determination in the previously issued LOMC. For LOMCs issued for multiple lots or structures where the determination for one or more of the lots or structures has changed, the LOMC cannot be revalidated through this administrative process. The NSP will review the data previously submitted for the LOMR or LOMA request and issue a new determination for the affected properties after the effective date of the revised FIRM. |

| Zone A | The flood insurance rate zone that corresponds to the 100-year floodplains that are determined in the FIS by approximate methods. Because detailed hydraulic analyses are not performed for such areas, no base flood elevations or depths are shown within this zone. | |

| Zone A99 | The flood insurance rate zone that corresponds to areas of the 100-year floodplain what will be protected by a Federal flood protection system where construction has reached specified statutory milestones. No base flood elevations or depths are shown within this zone. | |

| Zone AE | The flood insurance rate zone that corresponds to the 100-year floodplains that are determined in the FIS by detailed methods. In most instances, whole-foot base flood elevations derived from the detailed hydraulic analyses are shown at selected intervals within this zone. | |

| Zone AH | The flood insurance rate zone that corresponds to the 100-year shallow flooding (usually areas of ponding) where average depths are between 1 and 3 feet. Whole-foot base flood elevations are derived from detailed hydraulic analyses are shown at selected intervals within this zone. | |

| Zone AO | The flood insurance rate zone that corresponds to the 100-year shallow flooding ( usually sheet flow on sloping terrain) where average depths are between 1 and 3 feet. Average whole-foot depths derived from the detailed hydraulic analyses. The highest top of curb elevation adjacent to the lowest adjacent grade (LAG) must be submitted if the request lies within this zone. | |

| Zone AR | Zone AR is the flood insurance rate zone used to depict areas protected from flood hazards by flood control structures, such as a levee, that are being restored. FEMA will consider using the Zone AR designation for a community if the flood protection system has been deemed restorable by a Federal agency in consultation with a local project sponsor; a minimum level of flood protection is still provided to the community by the system; and restoration of the flood protection system is scheduled to begin within a designated time period and in accordance with a progress plan negotiated between the community and FEMA. Mandatory purchase requirements for flood insurance will apply in Zone AR, but the rate will not exceed the rate for unnumbered A zones if the structure is built in compliance with Zone AR floodplain management regulations. For floodplain management in Zone AR areas, elevation is not required for improvements to existing structures. However, for new construction, the structure must be elevated (or floodproofed for non-residential structures) such that the lowest floor, including basement, is a maximum of 3 feet above the highest adjacent existing grade if the depth of the base flood elevation (BFE) does not exceed 5 feet at the proposed development site. For infill sites, rehabilitation of existing structures, or redevelopment of previously developed areas, there is a 3 foot elevation requirement regardless of the depth of the BFE at the project site. The Zone AR designation will be removed and the restored flood control system shown as providing protection from the 1% annual chance flood on the NFIP map upon completion of the restoration project and submittal of all the necessary data to FEMA. | |

| Zone D | The flood insurance rate zone that corresponds to unstudied areas where flood hazards are undetermined but possible. | |

| Zone Gutter | Boundary, shown on a Flood Insurance Rate Map, dividing Special Flood Hazard Areas of different Base Flood Elevations, base flood depths, flood velocities, or flood insurance risk zone designations. | |

| Zone V | The flood insurance rate zone that corresponds to the 100-year costal floodplains that have additional hazards associated with storm waves. Because approximate hydraulic analyses are performed for such areas, no base flood elevations (BFEs) are shown within this zone. Mandatory flood insurance purchase requirements apply. | |

| Zone VE | Zone VE is the flood insurance rate zone that corresponds to the 100-year coastal floodplains that have additional hazards associated with storm waves. BFEs derived from the detailed hydraulic analyses are shown at selected intervals within this zone. Mandatory flood insurance purchase requirements apply. | |

| Zone X | The flood insurance rate zone that corresponds to areas outside the 500-year floodplain, areas within the 500- year floodplain, and areas of 100-year flooding where average depths are less than 1 foot, areas of 100-year flooding where the contributing drainage area is less than 1 square mile, and areas protected from 100-year flood by levees. No base flood elevations or depths are shown within this zone. | |

| Zone X (shaded and unshaded) B, and C | Are the flood insurance rate zones that corresponds to areas outside the 500-year floodplain, areas within the 500- year floodplain, and areas of 100-year flooding where average depths are less than 1 foot, areas of 100-year flooding where the contributing drainage area is less than 1 square mile, and areas protected from 100-year flood by levees. No base flood elevations or depths are shown within these zones. |

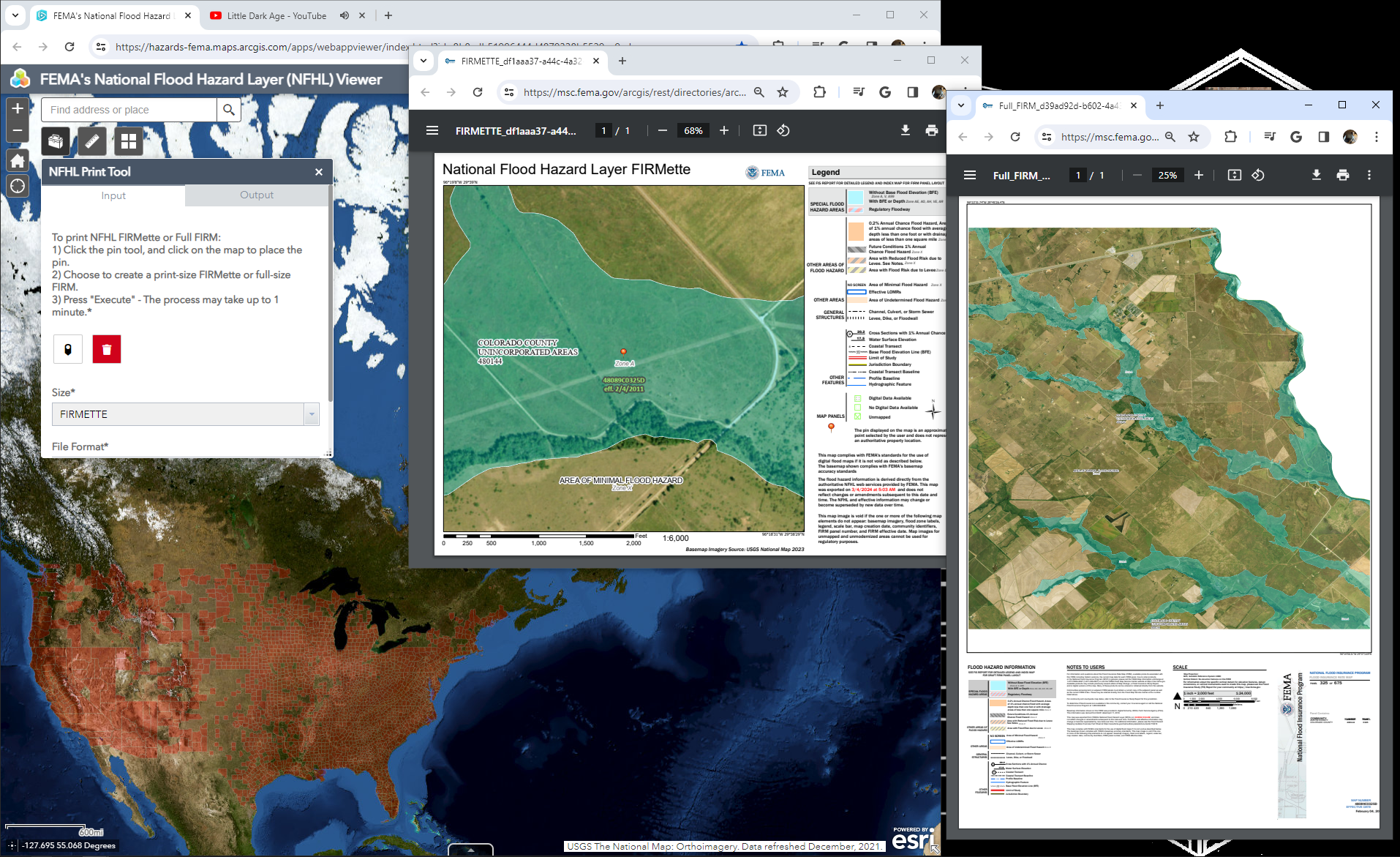

FIRMS - Flood Insurance Rate Maps

Water

Operational

FIM

Flood Insurance Rate Maps from FEMA are used to enforce flood insurance policy across the nation.

Back to Data Sources

Background and interpretation

As a regulatory product, the use and goals of these maps and data are no longer parallel to those of the hydraulic modeler, but they can help add some context to the underlying values and objectives of the communities they govern. Many of these maps are the result of taking the Base Level Engineering model outputs for a 1:100 year storm and mapping the elevation as the Base Flood Elevation. Further refinement “based on stakeholder input” are taken into account and the resultant map is accepted as the defacto standard off which flood insurance rates are set and enforced. These maps can display many different areas, but the ones of most common consequence include:

- High-Risk Zones (A & V): These areas are delineate as having the potential to inundate at least once every 100 years, or a 1% annual chance of experiencing a flood event (Sometimes also termed as Annual Exceedance Probability). These maps are the result of the elevations calculated from hydraulic models and the “base flood” that defines it are the zones under which federally backed mortgages must have some form of flood insurance. Zone V is used in coastal zones to indicate the area is impacted by wave action in addition to fluvial flooding.

- Moderate and Low-Risk Zones (X, B, C): These areas define locations which flood less frequently, and specific categories are called out on the FIRM legends. While not all are present for a given area, some of the more commonly found include Zone X (a 0.2% annual chance of flooding, once every 500 years), and medium to low risk zones such as B and C.

A table of zone definitions aggregated from FEMA Directory (n.d.). See the glossary for more definitions.

| Zone | Interpretation |

|---|---|

| A | The flood insurance rate zone that corresponds to the 100-year floodplains that are determined in the FIS by approximate methods. Because detailed hydraulic analyses are not performed for such areas, no base flood elevations or depths are shown within this zone. |

| AE | The flood insurance rate zone that corresponds to the 100-year floodplains that are determined in the FIS by detailed methods. In most instances, whole-foot base flood elevations derived from the detailed hydraulic analyses are shown at selected intervals within this zone. |

| AH | The flood insurance rate zone that corresponds to the 100-year shallow flooding (usually areas of ponding) where average depths are between 1 and 3 feet. Whole-foot base flood elevations are derived from detailed hydraulic analyses are shown at selected intervals within this zone. |

| AR | The flood insurance rate zone used to depict areas protected from flood hazards by flood control structures, such as a levee, that are being restored. FEMA will consider using the Zone AR designation for a community if the flood protection system has been deemed restorable by a Federal agency in consultation with a local project sponsor; a minimum level of flood protection is still provided to the community by the system; and restoration of the flood protection system is scheduled to begin within a designated time period and in accordance with a progress plan negotiated between the community and FEMA. Mandatory purchase requirements for flood insurance will apply in Zone AR, but the rate will not exceed the rate for unnumbered A zones if the structure is built in compliance with Zone AR floodplain management regulations. For floodplain management in Zone AR areas, elevation is not required for improvements to existing structures. However, for new construction, the structure must be elevated (or floodproofed for non-residential structures) such that the lowest floor, including basement, is a maximum of 3 feet above the highest adjacent existing grade if the depth of the base flood elevation (BFE) does not exceed 5 feet at the proposed development site. For infill sites, rehabilitation of existing structures, or redevelopment of previously developed areas, there is a 3 foot elevation requirement regardless of the depth of the BFE at the project site. The Zone AR designation will be removed and the restored flood control system shown as providing protection from the 1% annual chance flood on the NFIP map upon completion of the restoration project and submittal of all the necessary data to FEMA. |

| AO | The flood insurance rate zone that corresponds to the 100-year shallow flooding ( usually sheet flow on sloping terrain) where average depths are between 1 and 3 feet. Average whole-foot depths derived from the detailed hydraulic analyses. The highest top of curb elevation adjacent to the lowest adjacent grade (LAG) must be submitted if the request lies within this zone. |

| A99 | The flood insurance rate zone that corresponds to areas of the 100-year floodplain what will be protected by a Federal flood protection system where construction has reached specified statutory milestones. No base flood elevations or depths are shown within this zone. |

| D | The flood insurance rate zone that corresponds to unstudied areas where flood hazards are undetermined but possible. |

| Gutter | Boundary, shown on a Flood Insurance Rate Map, dividing Special Flood Hazard Areas of different Base Flood Elevations, base flood depths, flood velocities, or flood insurance risk zone designations. |

| V | The flood insurance rate zone that corresponds to the 100-year coastal floodplains that have additional hazards associated with storm waves. Because approximate hydraulic analyses are performed for such areas, no base flood elevations (BFEs) are shown within this zone. Mandatory flood insurance purchase requirements apply. |

| VE | The flood insurance rate zone that corresponds to the 100-year coastal floodplains that have additional hazards associated with storm waves. BFEs derived from the detailed hydraulic analyses are shown at selected intervals within this zone. Mandatory flood insurance purchase requirements apply. |

| X | The flood insurance rate zone that corresponds to areas outside the 500-year floodplain, areas within the 500- year floodplain, and areas of 100-year flooding where average depths are less than 1 foot, areas of 100-year flooding where the contributing drainage area is less than 1 square mile, and areas protected from 100-year flood by levees. No base flood elevations or depths are shown within this zone. |

| X (shaded and unshaded) B, and C | The flood insurance rate zones that corresponds to areas outside the 500-year floodplain, areas within the 500- year floodplain, and areas of 100-year flooding where average depths are less than 1 foot, areas of 100-year flooding where the contributing drainage area is less than 1 square mile, and areas protected from 100-year flood by levees. No base flood elevations or depths are shown within these zones. |

Aside: Modifications to these maps

If you want to build in these zones or have a property reevaluated for flood insurance purposes, there are two primary ways to go about accomplishing that. You can either receive a Letter of Map amendment, or a Letter of map Revision. LOMA’s “A Letter of Map Amendment (LOMA) is an official amendment, by letter, to an effective NFIP map. A LOMA establishes a property’s location in relation to the SFHA.” A Letter of Map Revision (LOMR) “is an official revision, by letter, to an effective NFIP map. A LOMR may change flood insurance risk zones, floodplain and/or floodway boundary delineations, planimetric features, and/or BFE.”

Aside: Blending use cases

As I allude to, I do not classify FIRM’s as a FIM product. This is a function of both my relative “power (ab)user” skillset and how these maps are used across the country. While FIRMS represent the “best available information” for a large swath of the country, there are locations which have neither product, there are locations which have both standard BLE models and FIRMS, and there are locations which have heavy invested in custom hydraulic modeling. None of these different data products will align perfectly. Additionally, much like all “federal” regulations, these set that minimum baseline, but states and counties may opt to adopt more rigorous standards. The standard “better practice” as used now is to compare both and use whichever has the most extent as an informed recommendation. It’s important to note however, that the FIRM extent takes legal precedent in enforcement, even if an alternative model shows greater extents.

Aside: Disaster recovery and payouts

One of the commonly used metrics in the use of these flood insurance programs and the National Flood Insurance Program is the 50% rule. If a building is flooded, insurance payouts can occur in a few different ways. If a building is historic, the renovations may take place but for every dollar spent, a match in flood prevention measures must take place. If the building is not historic and is more than 50% destroyed, renovations must also include bringing the structure back up to code. Enforcement and interpretation is up to the states, FEMA, flood insurance providers, and the lawyers. I just like making the maps and the design of the structures.

Sources: https://sarasota.wateratlas.usf.edu/upload/documents/FloodplainFacts.pdf https://www.fema.gov/pdf/nfip/manual201205/content/16_maps.pdf https://adeca.alabama.gov/faq/what-are-the-different-types-of-letters-of-map-change-lomcs/#:~:text=LOMA%20%E2%80%93%20A%20Letter%20of%20Map,to%20an%20effective%20NFIP%20map.

References

FEMA Directory. n.d. Https://hazards.fema.gov/femaportal/wps/portal/!ut/p/z0/04_Sj9CPykssy0xPLMnMz0vMAfIjo8zifQI83D38vQ38DdyCLQ0CnY1djAN9TY0NzAz0C7IdFQHJLwc3/.